statsmodels.stats.stattools.robust_skewness¶

-

statsmodels.stats.stattools.robust_skewness(y, axis=0)[source]¶ Calculates the four skewness measures in Kim & White

Parameters: y : array-like

axis : int or None, optional

Axis along which the skewness measures are computed. If None, the entire array is used.

Returns: sk1 : ndarray

The standard skewness estimator.

sk2 : ndarray

Skewness estimator based on quartiles.

sk3 : ndarray

Skewness estimator based on mean-median difference, standardized by absolute deviation.

sk4 : ndarray

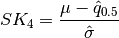

Skewness estimator based on mean-median difference, standardized by standard deviation.

Notes

The robust skewness measures are defined

![SK_{3}=\frac{\mu-\hat{q}_{0.5}}

{\hat{E}\left[\left|y-\hat{\mu}\right|\right]}](../_images/math/339e3615d9d259f5d8ea27391108f87e9916b8c5.png)

[R59] Tae-Hwan Kim and Halbert White, “On more robust estimation of skewness and kurtosis,” Finance Research Letters, vol. 1, pp. 56-73, March 2004.