Regression diagnostics¶

This example file shows how to use a few of the statsmodels regression diagnostic tests in a real-life context. You can learn about more tests and find out more information about the tests here on the Regression Diagnostics page.

Note that most of the tests described here only return a tuple of numbers, without any annotation. A full description of outputs is always included in the docstring and in the online statsmodels documentation. For presentation purposes, we use the zip(name,test) construct to pretty-print short descriptions in the examples below.

Estimate a regression model¶

[1]:

%matplotlib inline

[2]:

from statsmodels.compat import lzip

import numpy as np

import pandas as pd

import statsmodels.formula.api as smf

import statsmodels.stats.api as sms

import matplotlib.pyplot as plt

# Load data

url = "https://raw.githubusercontent.com/vincentarelbundock/Rdatasets/master/csv/HistData/Guerry.csv"

dat = pd.read_csv(url)

# Fit regression model (using the natural log of one of the regressors)

results = smf.ols("Lottery ~ Literacy + np.log(Pop1831)", data=dat).fit()

# Inspect the results

print(results.summary())

OLS Regression Results

==============================================================================

Dep. Variable: Lottery R-squared: 0.348

Model: OLS Adj. R-squared: 0.333

Method: Least Squares F-statistic: 22.20

Date: Fri, 05 Dec 2025 Prob (F-statistic): 1.90e-08

Time: 18:10:32 Log-Likelihood: -379.82

No. Observations: 86 AIC: 765.6

Df Residuals: 83 BIC: 773.0

Df Model: 2

Covariance Type: nonrobust

===================================================================================

coef std err t P>|t| [0.025 0.975]

-----------------------------------------------------------------------------------

Intercept 246.4341 35.233 6.995 0.000 176.358 316.510

Literacy -0.4889 0.128 -3.832 0.000 -0.743 -0.235

np.log(Pop1831) -31.3114 5.977 -5.239 0.000 -43.199 -19.424

==============================================================================

Omnibus: 3.713 Durbin-Watson: 2.019

Prob(Omnibus): 0.156 Jarque-Bera (JB): 3.394

Skew: -0.487 Prob(JB): 0.183

Kurtosis: 3.003 Cond. No. 702.

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

Normality of the residuals¶

Jarque-Bera test:

[3]:

name = ["Jarque-Bera", "Chi^2 two-tail prob.", "Skew", "Kurtosis"]

test = sms.jarque_bera(results.resid)

lzip(name, test)

[3]:

[('Jarque-Bera', np.float64(3.39360802484318)),

('Chi^2 two-tail prob.', np.float64(0.18326831231663254)),

('Skew', np.float64(-0.4865803431122347)),

('Kurtosis', np.float64(3.003417757881634))]

Omni test:

[4]:

name = ["Chi^2", "Two-tail probability"]

test = sms.omni_normtest(results.resid)

lzip(name, test)

[4]:

[('Chi^2', np.float64(3.7134378115971933)),

('Two-tail probability', np.float64(0.15618424580304735))]

Influence tests¶

Once created, an object of class OLSInfluence holds attributes and methods that allow users to assess the influence of each observation. For example, we can compute and extract the first few rows of DFbetas by:

[5]:

from statsmodels.stats.outliers_influence import OLSInfluence

test_class = OLSInfluence(results)

test_class.dfbetas[:5, :]

[5]:

array([[-0.00301154, 0.00290872, 0.00118179],

[-0.06425662, 0.04043093, 0.06281609],

[ 0.01554894, -0.03556038, -0.00905336],

[ 0.17899858, 0.04098207, -0.18062352],

[ 0.29679073, 0.21249207, -0.3213655 ]])

Explore other options by typing dir(influence_test)

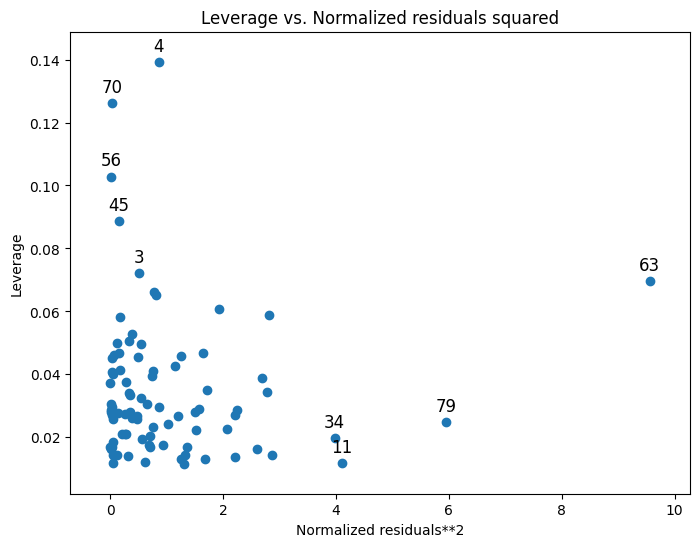

Useful information on leverage can also be plotted:

[6]:

from statsmodels.graphics.regressionplots import plot_leverage_resid2

fig, ax = plt.subplots(figsize=(8, 6))

fig = plot_leverage_resid2(results, ax=ax)

Other plotting options can be found on the Graphics page.

Multicollinearity¶

Condition number:

[7]:

np.linalg.cond(results.model.exog)

[7]:

np.float64(702.1792145490066)

Heteroskedasticity tests¶

Breush-Pagan test:

[8]:

name = ["Lagrange multiplier statistic", "p-value", "f-value", "f p-value"]

test = sms.het_breuschpagan(results.resid, results.model.exog)

lzip(name, test)

[8]:

[('Lagrange multiplier statistic', np.float64(4.893213374094005)),

('p-value', np.float64(0.08658690502352002)),

('f-value', np.float64(2.5037159462564618)),

('f p-value', np.float64(0.08794028782672814))]

Goldfeld-Quandt test

[9]:

name = ["F statistic", "p-value"]

test = sms.het_goldfeldquandt(results.resid, results.model.exog)

lzip(name, test)

[9]:

[('F statistic', np.float64(1.1002422436378143)),

('p-value', np.float64(0.38202950686925324))]

Linearity¶

Harvey-Collier multiplier test for Null hypothesis that the linear specification is correct:

[10]:

name = ["t value", "p value"]

test = sms.linear_harvey_collier(results)

lzip(name, test)

[10]:

[('t value', np.float64(-1.0796490077759802)),

('p value', np.float64(0.2834639247569222))]