Estimating or specifying parameters in state space models#

In this notebook we show how to fix specific values of certain parameters in statsmodels’ state space models while estimating others.

In general, state space models allow users to:

Estimate all parameters by maximum likelihood

Fix some parameters and estimate the rest

Fix all parameters (so that no parameters are estimated)

[1]:

%matplotlib inline

import matplotlib.pyplot as plt

import pandas as pd

from pandas_datareader.data import DataReader

import statsmodels.api as sm

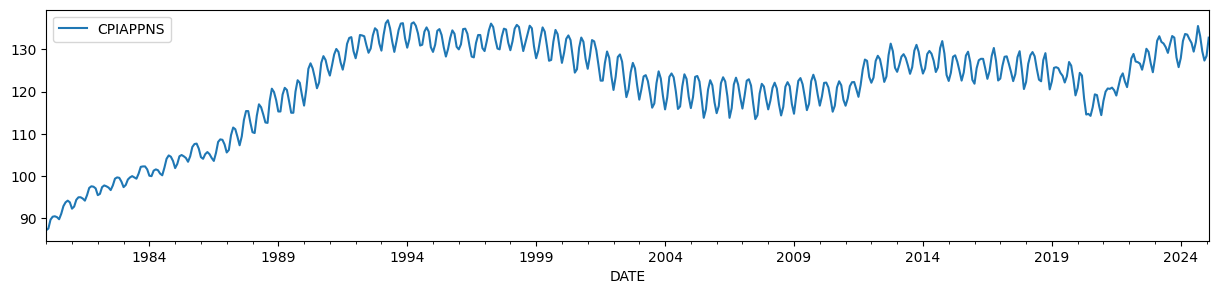

To illustrate, we will use the Consumer Price Index for Apparel, which has a time-varying level and a strong seasonal component.

[2]:

endog = DataReader("CPIAPPNS", "fred", start="1980").asfreq("MS")

endog.plot(figsize=(15, 3));

It is well known (e.g. Harvey and Jaeger [1993]) that the HP filter output can be generated by an unobserved components model given certain restrictions on the parameters.

The unobserved components model is:

For the trend to match the output of the HP filter, the parameters must be set as follows:

where \(\lambda\) is the parameter of the associated HP filter. For the monthly data that we use here, it is usually recommended that \(\lambda = 129600\).

[3]:

# Run the HP filter with lambda = 129600

hp_cycle, hp_trend = sm.tsa.filters.hpfilter(endog, lamb=129600)

# The unobserved components model above is the local linear trend, or "lltrend", specification

mod = sm.tsa.UnobservedComponents(endog, "lltrend")

print(mod.param_names)

['sigma2.irregular', 'sigma2.level', 'sigma2.trend']

The parameters of the unobserved components model (UCM) are written as:

\(\sigma_\varepsilon^2 = \text{sigma2.irregular}\)

\(\sigma_\eta^2 = \text{sigma2.level}\)

\(\sigma_\zeta^2 = \text{sigma2.trend}\)

To satisfy the above restrictions, we will set \((\sigma_\varepsilon^2, \sigma_\eta^2, \sigma_\zeta^2) = (1, 0, 1 / 129600)\).

Since we are fixing all parameters here, we do not need to use the fit method at all, since that method is used to perform maximum likelihood estimation. Instead, we can directly run the Kalman filter and smoother at our chosen parameters using the smooth method.

[4]:

res = mod.smooth([1.0, 0, 1.0 / 129600])

print(res.summary())

Unobserved Components Results

==============================================================================

Dep. Variable: CPIAPPNS No. Observations: 558

Model: local linear trend Log Likelihood -3111.849

Date: Thu, 30 Jul 2026 AIC 6229.697

Time: 06:42:18 BIC 6242.660

Sample: 01-01-1980 HQIC 6234.761

- 06-01-2026

Covariance Type: opg

====================================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------------

sigma2.irregular 1.0000 0.008 119.838 0.000 0.984 1.016

sigma2.level 0 0.000 0 1.000 -0.000 0.000

sigma2.trend 7.716e-06 1.82e-07 42.297 0.000 7.36e-06 8.07e-06

===================================================================================

Ljung-Box (L1) (Q): 262.14 Jarque-Bera (JB): 2.01

Prob(Q): 0.00 Prob(JB): 0.37

Heteroskedasticity (H): 1.98 Skew: 0.04

Prob(H) (two-sided): 0.00 Kurtosis: 2.72

===================================================================================

Warnings:

[1] Covariance matrix calculated using the outer product of gradients (complex-step).

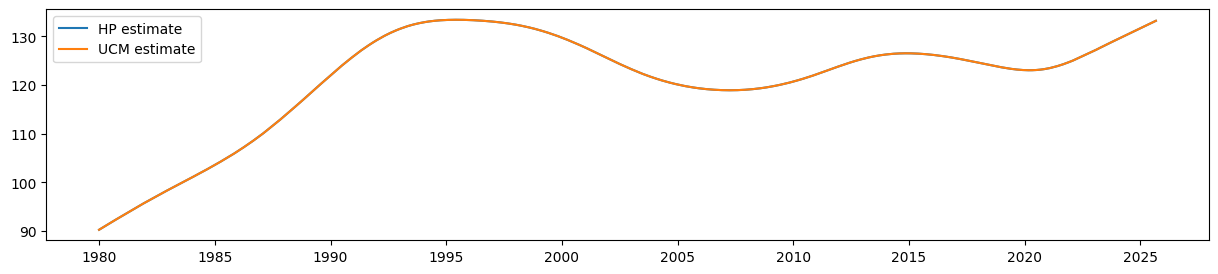

The estimate that corresponds to the HP filter’s trend estimate is given by the smoothed estimate of the level (which is \(\mu_t\) in the notation above):

[5]:

ucm_trend = pd.Series(res.level.smoothed, index=endog.index)

It is easy to see that the estimate of the smoothed level from the UCM is equal to the output of the HP filter:

[6]:

fig, ax = plt.subplots(figsize=(15, 3))

ax.plot(hp_trend, label="HP estimate")

ax.plot(ucm_trend, label="UCM estimate")

ax.legend();

Adding a seasonal component#

However, unobserved components models are more flexible than the HP filter. For example, the data shown above is clearly seasonal, but with time-varying seasonal effects (the seasonality is much weaker at the beginning than at the end). One of the benefits of the unobserved components framework is that we can add a stochastic seasonal component. In this case, we will estimate the variance of the seasonal component by maximum likelihood while still including the restriction on the parameters implied above so that the trend corresponds to the HP filter concept.

Adding the stochastic seasonal component adds one new parameter, sigma2.seasonal.

[7]:

# Construct a local linear trend model with a stochastic seasonal component of period 1 year

mod = sm.tsa.UnobservedComponents(

endog, "lltrend", seasonal=12, stochastic_seasonal=True

)

print(mod.param_names)

['sigma2.irregular', 'sigma2.level', 'sigma2.trend', 'sigma2.seasonal']

In this case, we will continue to restrict the first three parameters as described above, but we want to estimate the value of sigma2.seasonal by maximum likelihood. Therefore, we will use the fit method along with the fix_params context manager.

The fix_params method takes a dictionary of parameters names and associated values. Within the generated context, those parameters will be used in all cases. In the case of the fit method, only the parameters that were not fixed will be estimated.

[8]:

# Here we restrict the first three parameters to specific values

with mod.fix_params(

{"sigma2.irregular": 1, "sigma2.level": 0, "sigma2.trend": 1.0 / 129600}

):

# Now we fit any remaining parameters, which in this case

# is just `sigma2.seasonal`

res_restricted = mod.fit()

Alternatively, we could have simply used the fit_constrained method, which also accepts a dictionary of constraints:

[9]:

res_restricted = mod.fit_constrained(

{"sigma2.irregular": 1, "sigma2.level": 0, "sigma2.trend": 1.0 / 129600}

)

The summary output includes all parameters, but indicates that the first three were fixed (and so were not estimated).

[10]:

print(res_restricted.summary())

Unobserved Components Results

=====================================================================================

Dep. Variable: CPIAPPNS No. Observations: 558

Model: local linear trend Log Likelihood -1793.098

+ stochastic seasonal(12) AIC 3588.196

Date: Thu, 30 Jul 2026 BIC 3592.497

Time: 06:42:20 HQIC 3589.877

Sample: 01-01-1980

- 06-01-2026

Covariance Type: opg

============================================================================================

coef std err z P>|z| [0.025 0.975]

--------------------------------------------------------------------------------------------

sigma2.irregular (fixed) 1.0000 nan nan nan nan nan

sigma2.level (fixed) 0 nan nan nan nan nan

sigma2.trend (fixed) 7.716e-06 nan nan nan nan nan

sigma2.seasonal 0.0962 0.008 12.761 0.000 0.081 0.111

===================================================================================

Ljung-Box (L1) (Q): 476.69 Jarque-Bera (JB): 42.96

Prob(Q): 0.00 Prob(JB): 0.00

Heteroskedasticity (H): 2.24 Skew: 0.32

Prob(H) (two-sided): 0.00 Kurtosis: 4.22

===================================================================================

Warnings:

[1] Covariance matrix calculated using the outer product of gradients (complex-step).

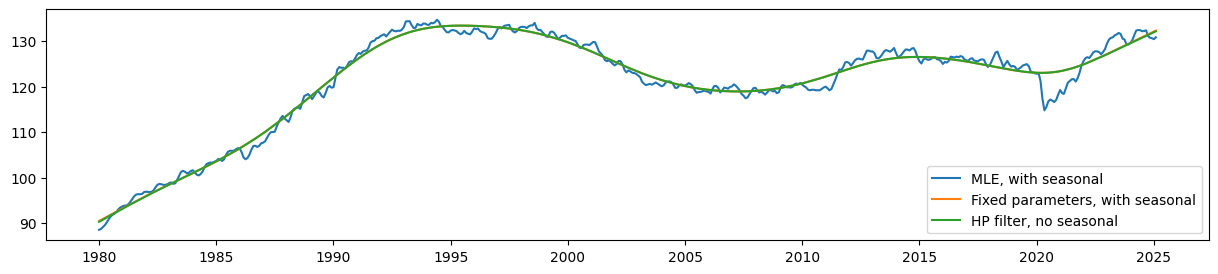

For comparison, we construct the unrestricted maximum likelihood estimates (MLE). In this case, the estimate of the level will no longer correspond to the HP filter concept.

[11]:

res_unrestricted = mod.fit()

Finally, we can retrieve the smoothed estimates of the trend and seasonal components.

[12]:

# Construct the smoothed level estimates

unrestricted_trend = pd.Series(res_unrestricted.level.smoothed, index=endog.index)

restricted_trend = pd.Series(res_restricted.level.smoothed, index=endog.index)

# Construct the smoothed estimates of the seasonal pattern

unrestricted_seasonal = pd.Series(res_unrestricted.seasonal.smoothed, index=endog.index)

restricted_seasonal = pd.Series(res_restricted.seasonal.smoothed, index=endog.index)

Comparing the estimated level, it is clear that the seasonal UCM with fixed parameters still produces a trend that corresponds very closely (although no longer exactly) to the HP filter output.

Meanwhile, the estimated level from the model with no parameter restrictions (the MLE model) is much less smooth than these.

[13]:

fig, ax = plt.subplots(figsize=(15, 3))

ax.plot(unrestricted_trend, label="MLE, with seasonal")

ax.plot(restricted_trend, label="Fixed parameters, with seasonal")

ax.plot(hp_trend, label="HP filter, no seasonal")

ax.legend();

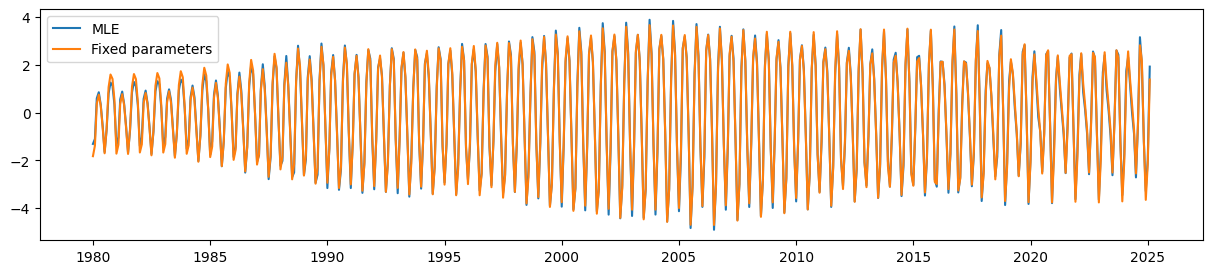

Finally, the UCM with the parameter restrictions is still able to pick up the time-varying seasonal component quite well.

[14]:

fig, ax = plt.subplots(figsize=(15, 3))

ax.plot(unrestricted_seasonal, label="MLE")

ax.plot(restricted_seasonal, label="Fixed parameters")

ax.legend();